Your Finances. Your Family. Your Future.

We're here to help!

720-366-9514

Strategically Personalized Framework

This page is designed to provide a more in-depth understanding of the following:

-

Why we developed the Strategically Personalized Framework (SPF) solution.

-

How it compares to "the other guys" retirement solutions.

-

Understanding how SPF is designed to work.

As you learn about our Strategically Personalized Framework solution & evaluate if it's right for you, feel free to use the contact form below with any questions you may have.

Key Features

AUM Fee: 1.00% (annually)

Min. Target: $750,000 (total portfolio value)

Required: Financial Plan (included in service)

Recession is a scary word. The Strategically Personalized Portfolio was born out of response to the 2008 Great Financial Crisis. Recessions are a normal cycle of modern economies. Since the Great Depression until the Covid-19 Pandemic the American economy has experienced 15 Recessions. We can't control when a recession occurs, but we can control how we prepare our finances for one. For some reason the industry wouldn't....and we couldn't figure out why.

Traditional money managers seem to focus on "efficiency" and "volume". Enter the "one portfolio solution". This efficiency focus creates an environment where clients are pigeonholed into one of three broad groups: Aggressive, Moderate, or Conservative. This is generally described as a client's "risk tolerance". These broad asset allocation portfolios certainly have a place in wealth management, it just isn't retirement in our humble opinions. Here are a couple of reasons why we don't feel it's the right strategy for retirees:

-

Income & Distributions

-

Sequence of Return Risk

-

The Emotional Realities of Investing

Below we'll look at each reason in more detail. Understanding these will better help you understand why we developed our Strategically Personalized Framework solution.

Retirees Deserve Better!

1

Income & Distributions

Your money has a risk tolerance too. Traditional money management makes this a secondary concern, but for retirees it's at the forefront of their minds. Your retirement portfolio is supposed to pay bills for the next 20+ years. Money that's paying for bills tomorrow should be invested very differently than money being used a decade from now. A "one portfolio" asset allocation solution isn't well suited for this. Why you ask? Because of their rebalancing process.

Most of these portfolios rebalance quarterly. Which means they sell & buy investments depending on their target exposure level. This means your monthly income is coming from a little bit of every investment you own. Some that are performing well & some that aren't. Preferred asset classes & out of favor asset classes. Even if the manager sells all of one investment type to send your income from, when the quarterly rebalance occurs they'll be buying it again. It'll just be temporary until each rebalance. If they didn't rebalance then your portfolio's risk would drift. This could result in having too aggressive or too conservative of a portfolio.

In a one portfolio asset allocation solution you don't have the flexibility to produce income from the right source at the best time given the economic conditions you're in. And those conditions always change, which means the best place to take income from will change also.

2

Sequence of Return Risk

Sequence of return risk is the risk that the order in which investment returns occur can impact how long retirement savings last. Here's an example from Schwab's Center for Financial Research:

If all of your funds are invested in a single portfolio solution then you are subject to the whims of market volatility. It's like driving a car without a seatbelt. No one thinks they'll get in a car accident, but we don't always have control over that. If circumstances beyond your control result in an accident...the damage that can occur without a seatbelt could change your family's lives forever. Retirees that use a portfolio solution that doesn't offer some protection against this risk aren't wearing a seatbelt and just hoping for the best. Hope isn't a strategy...

3

The Emotional Realities of Investing

Money is emotional. Making decisions about money is intimidating. Retirement is the pinnacle of this anxiety. During 2008 when retirees watched the news and saw headlines from the Wall Street Journal like "Worst Crisis Since '30s, with No End Yet in Sight", it was more than just dollars they saw disappearing. It was time with family. It was freedom. And all that replaced it was fear of the unknown... It's easy for financial talking heads to say, "Just hold on for the long-term" on television while earning millions every year. For the every day investor on main street its a different story.

Emotional decisions can lead to financial ruin. The industry's solution for this is to try and take the emotions out of the equation, but it's just not possible. People are emotional. Emotions are necessary for decision making. The solution shouldn't be to get people to stop being people. The solution should be protecting the portion of people's money that they're most immediately concerned about - the money for tomorrow's bills.

The 2008 Great Financial Crisis took roughly 48 months from start to finish. It took approximately 18 months from the market bottom to recover to it's starting value during the crisis. Most people remember what that period was like. Now imagine how different the crisis would have been for an individual that had 72 months worth of income strategically accounted for in a lower volatility, or lower risk, portfolio. Would you have panicked if that uncertainty didn't affect tomorrow's lifestyle?

PWM's Approach

Prosperity Wealth Management focuses on "flexibility" & "resiliency". That's where our Strategically Personalized Framework comes in. The SPF solution provides clients with the ability to source income in a way that isn't dictated by what the stock market is doing. It's also completely customized to your family's needs.

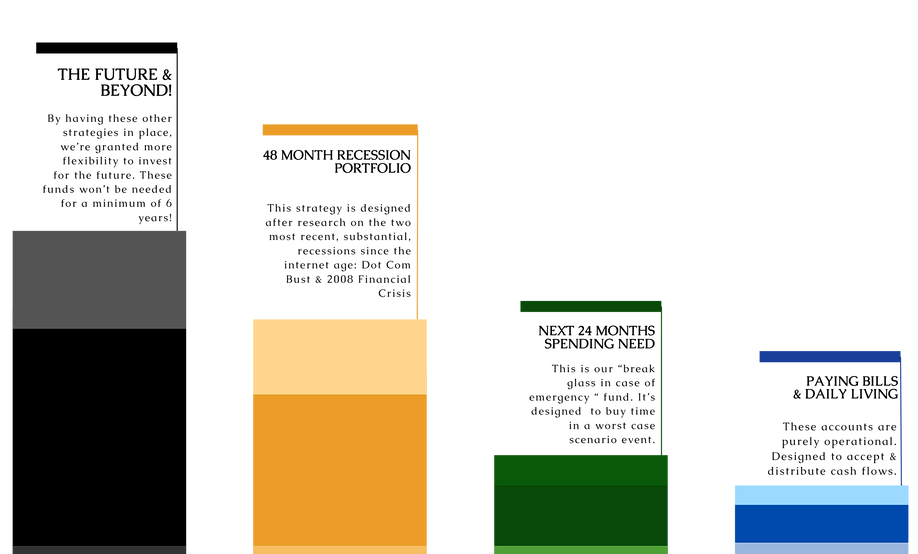

Here's how it works. After completing your financial plan we'll have a detailed understanding of what our expected spending is each year of retirement (we build in buffers for cushion). We then use these expected spending figures to build your financial structure. We believe each household should have three (3) portfolios. We've affectionately named them our Treasury, Prudent, & Expansion portfolios.

Our Treasury portfolio is composed of ultra safe, short-term, United States Government bonds. We recommend a minimum of the next 24 months of spending for this portfolio. Why 24 months? Because it took 18 months for markets to recover from their bottom in 2008. This is our seatbelt. Sure during a smooth peaceful ride having it could feel uncomfortable... but in the event of an accident you'll thank the heavens you had it.

Our Prudent portfolio is composed of high quality & low volatility investments. Think of these as the "old stalwart" investments of your father's day. The stock portion of the portfolio is characterized by large companies with strong brands & a loyal customer base. They'll typically pay dividends, and their prices fluctuate less than the broad market. The bond portion of the portfolio is investment grade & ranges from short (less than a year) to intermediate (approximately 6 years) term debt. We recommend a minimum of 48 months of spending in this portfolio. Think of this as the ship's ballast. It's not the flashiest part of the ship, but you're sure glad you have it when the storm waves come crashing.

Lastly, we have our Expansion portfolio. Because the rest of the framework is composed of your bank assets, the 24mo Treasury portfolio, and the 48mo Prudent portfolio, the Expansion portfolio can take more risks. Why? Because you've already stockpiled at least (remember its fully customizable) the next 72 months of your projected spending. That means you don't need to turn to this money for at least 6 years in the worst of circumstances. Arguably the best time to buy stocks, or riskier investments, in the modern era was at the bottom in 2008. Most people didn't have the flexibility or financial security to do that. With this framework in place, our Expansion portfolio does!

Remember how we said it's customizable? Personalized isn't in the name as a buzzword. Our 24-month Treasury and 48-month Prudent portfolios are minimum recommendations. Some clients need a little more security. As long as it works in your financial plan, it doesn't make a difference to us how much more you allocate to these portfolios. Some clients have asked for 10 year's worth of spending accounted for in our lower volatility portfolios. Great! Making sure you are comfortable with your exposure is how we protect clients from making permanent irreversible decisions.

It's important to understand that you live with the consequences of these decisions - no one else. Not your advisor. Not your friends. Only your family. When you take away the cloud of fear the stock market can enshroud people with, all that is left is opportunity. That is why we believe a strategic, personalized, and thoughtful financial framework is essential for the long-term success of our retired, and near retired, clients.

SPF Painpoints

Transparency is important. Part of our focus on being a wealth management firm of a new era is on making sure clients understand EVERYTHING about our solutions. To put your strategically personalized framework into place we have to jump through a few hoops. Here are the painpoints as we see them.

One, you'll be opening multiple accounts. We get it. The logistics of our business when it comes to forms, disclosures, and redundancies can be exhausting. We do our best to streamline this through our custodians digital onboarding platform.

Two, the solution isn't "set it and forget it". You'll need to be actively engaged with us. The amount we allocate to each portfolio will evolve with cost of living and your personal preferences. Sometimes you'll get a phone call that says, "We think now's a good time to pay for next year's vacation. We want your permission to send you some money" based on the market environment we're in. This isn't a solution for someone that wants zero involvement and no relationship.

Three, this is going to feel different. If you've worked with large financial institutions in the past, then you've had a very different experience. We're not fitting you into a mold that three hundred other clients are crammed into. You're helping us build a new mold that's right for your family. That's new and new can feel different.

Lastly, fees. We know we know, but we're not free. Part of our state regulations is we need to send out a billing statement separate from your normal monthly statements. Depending on if you elected for monthly or quarterly billing you could be getting pretty frequent reminders that you're paying for our service. Everything has a cost of doing business, but it's not always fun being constantly reminded of it.

Personalization

The ability to personalize your experience with us is a core value of our firm. That extends to every part of the client experience. This is a different approach from most of our competitors. You get to decide how, when, and with what frequency you want to hear from us. No part of working with us is set in stone. Every part is designed to evolve based on your preferences at that moment in time.

The Strategically Personalized Framework is designed to address the most common questions we get when clients approach retirement.

-

"Will I run out of money?"

-

"What happens if the 2008 Financial Crisis happens again?"

-

"How do I create a paycheck now that I'm done working?"

-

"What happens if something happens to me?"

The transition from a career into retirement is a stark and often difficult one. It takes months, if not years, to settle into a comfortable routine. Having an answer to each question above and knowing you're entering that next stage of life with a financial framework custom built for your family can make all the difference.

If you're interested in just one of the portfolios used in our Strategically Personalized Framework we are open to having that conversation with you. We'll still need to go through the financial planning process to ensure it's in your best interest. We mean it when we say the entire process is personalized for your family.

Contact us to start maximizing your financial flexibility!